2021 was a good year for housing starts in the U.S. In Canada, it was an outstanding year.

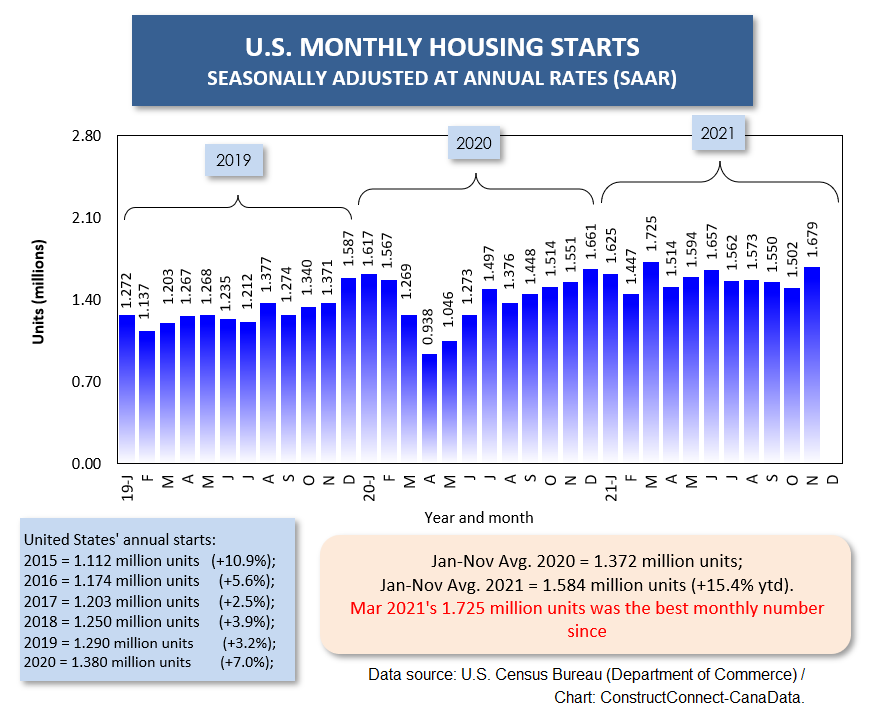

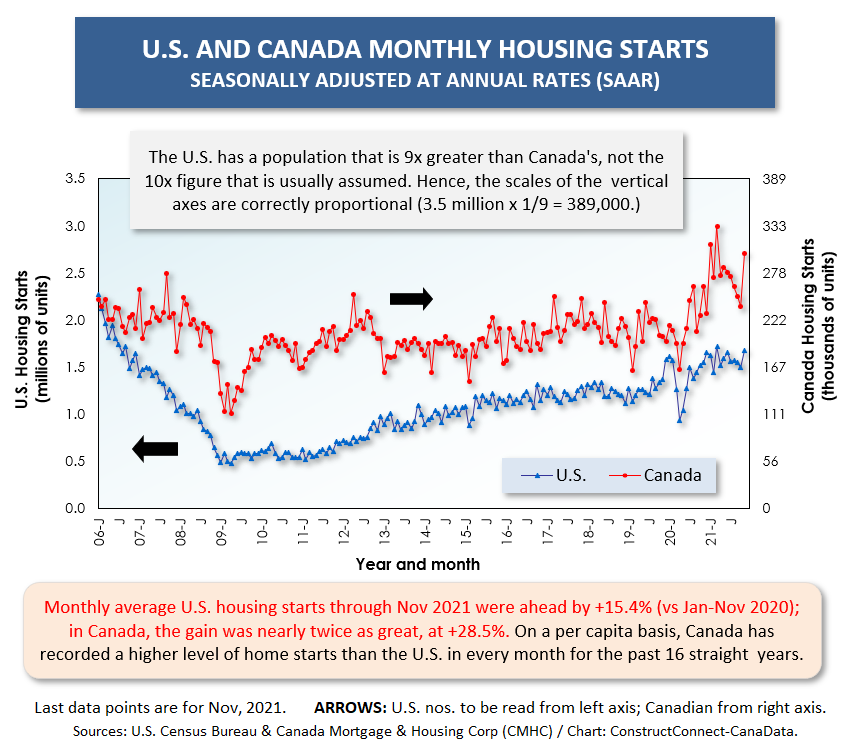

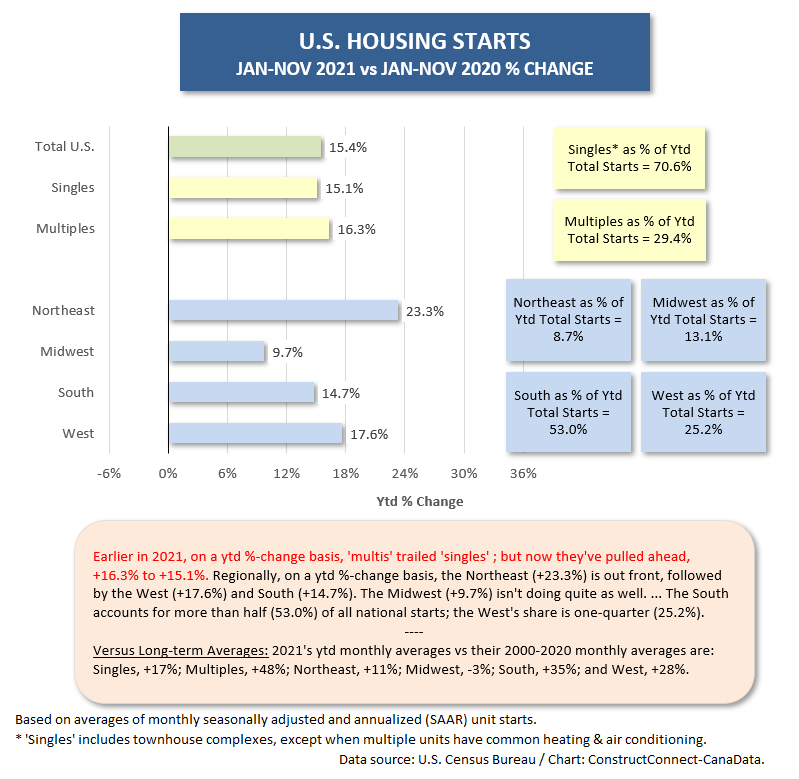

Through the first 11 months of 2021, in America, average monthly new home groundbreakings, seasonally adjusted at an annual rate (SAAR), were +15.4% versus January-November 2020.

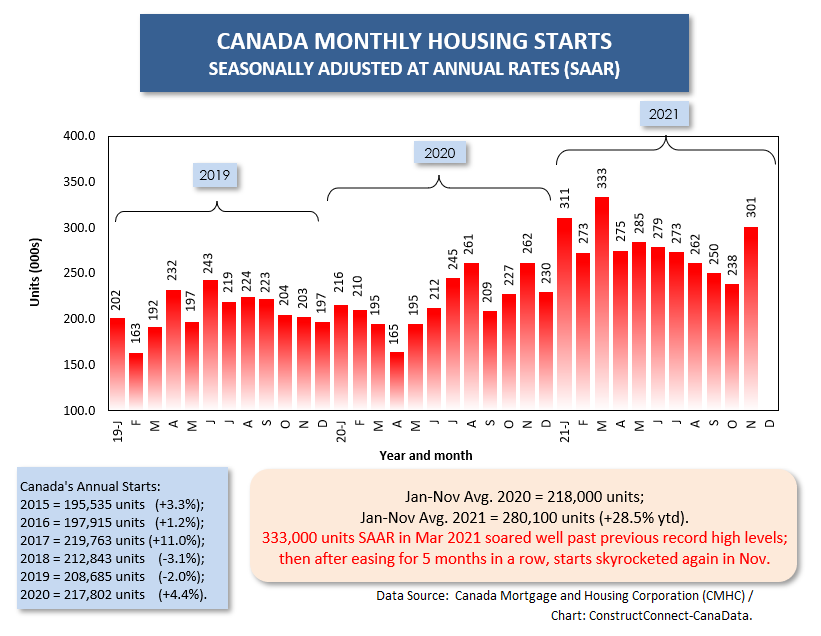

In Canada, the comparable percentage change was nearly twice as great, +28.5%.

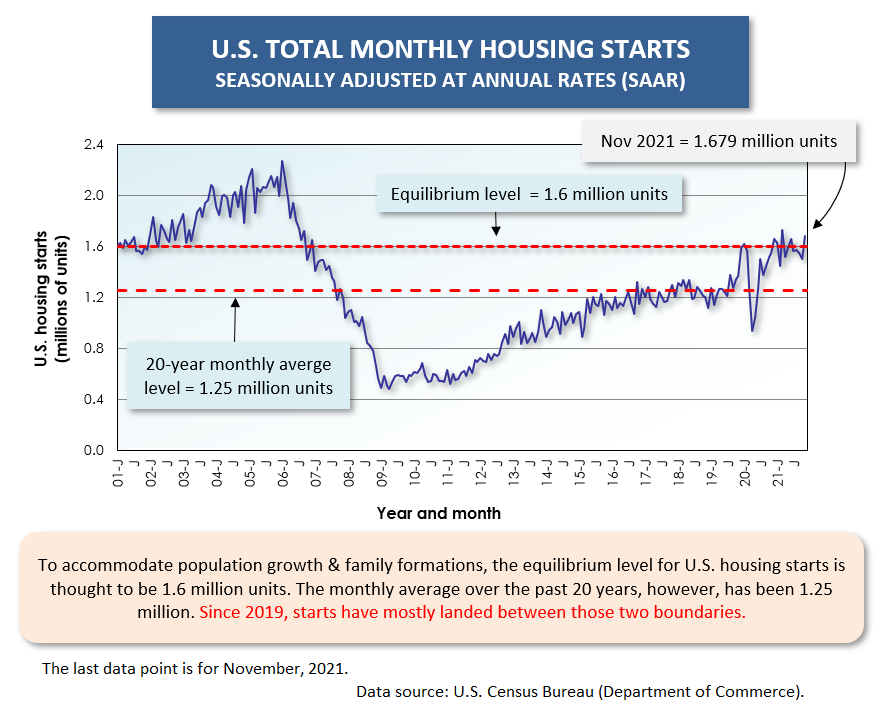

In March 2021, at 1.725 million units SAAR, the U.S. managed its highest level of housing starts in 15 years, dating back to 2006. (The U.S. all-time peak was 2.273 million units SAAR in January 2006).

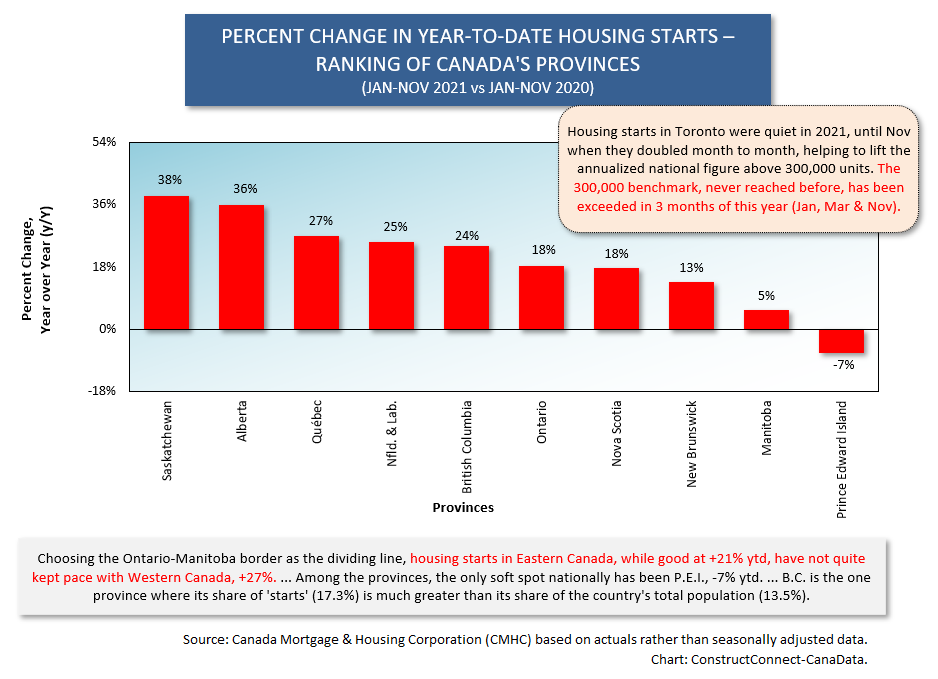

In March 2021, at 333,000 units, Canada attained an all-time highest level of housing starts.

Prior to 2021, the 300,000-milestone had never been surpassed. Climbing beyond 300,000 was achieved three times in the latest year, in January, March and, coming as a big surprise, again in November. (In the five months leading into November, Canadian housing starts were trending downwards.)

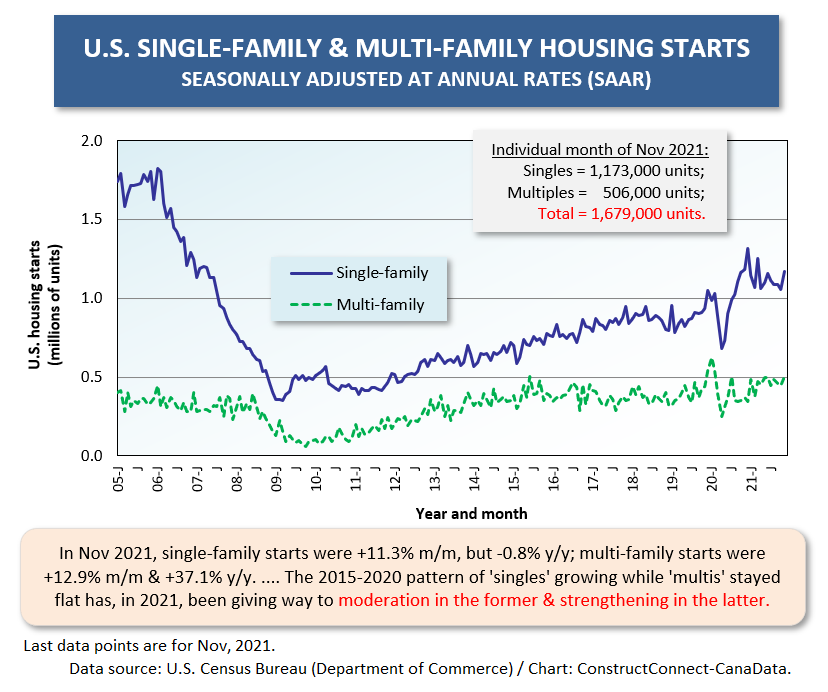

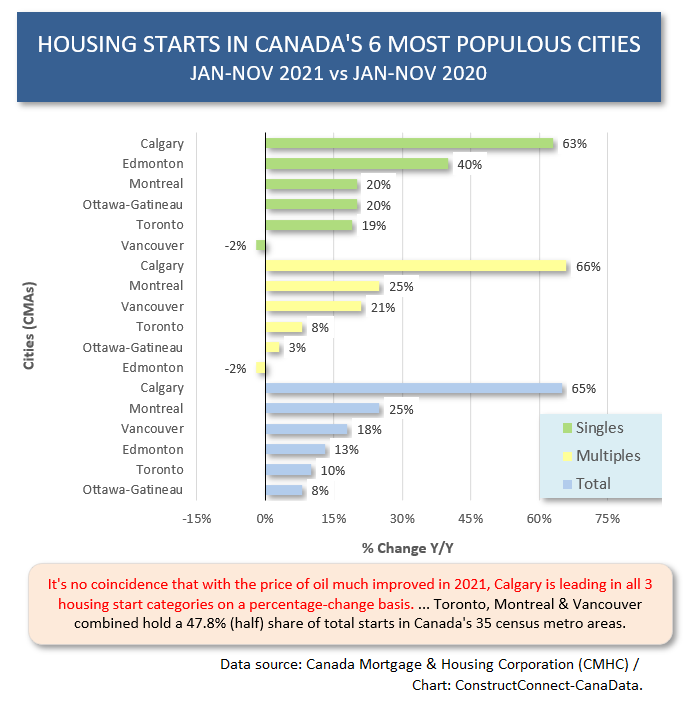

Recently, there’s been a reversal in the performances of single-family starts versus multi-family starts in the U.S. In the first part of 2021, the former was chalking up much larger year-over-year percentage gains than the latter. But now, the monthly average of multi-family starts is +16.3% year over year compared with a slightly lower +15.1% for single-family starts.

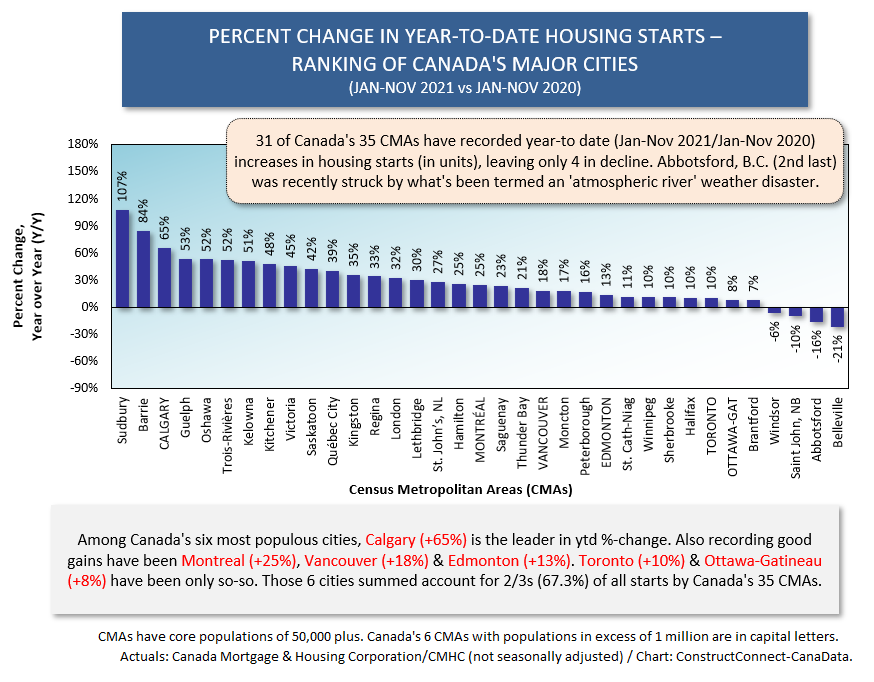

Among Canada’s 35 census metropolitan areas (CMAs), single-family starts are +26% year to date while multis are +21%.

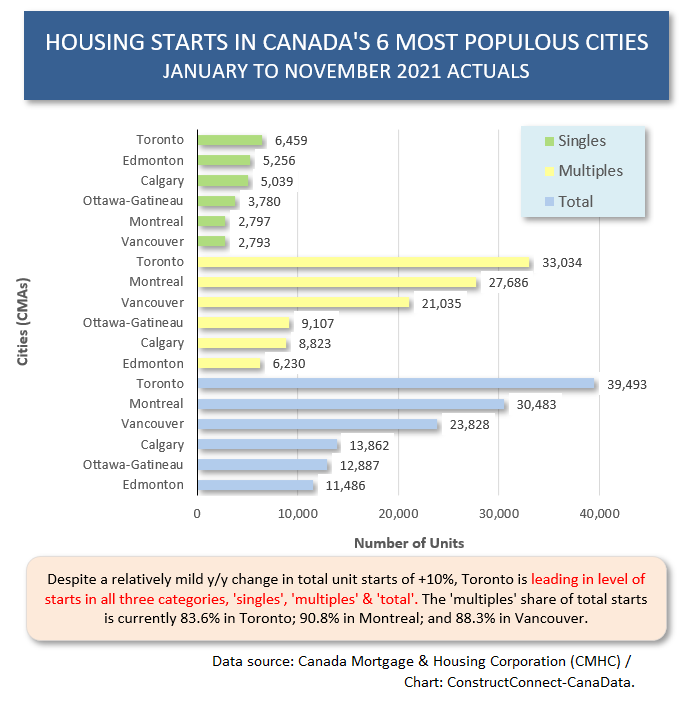

The proportion of total starts that are multis remains much lower in the U.S. than in Canada: ������about one-third south of the border; more than two-thirds north of the border.

The fact multi-unit housing starts in Toronto (Canada’s largest urban housing market) doubled month-to-month in November was a major reason total starts nation-wide once again shot up above 300,000 units.

With inflation coming out of its cave and terrorizing the townsfolk, there will almost surely be interest rate hikes in 2022, unless mounting coronavirus cases slow economic growth to the point where central banks won’t dare to tighten.

In the initial stages of interest rate increases, history has shown that demand does not tail off. Many potential buyers, who have been holding back, will jump into the marketplace, fearing they’ll be caught in more dire financing circumstances if they wait any longer.

Affordability will continue to be an issue. Existing home prices in both the U.S. and Canada are currently up by approximately a fifth year over year.

The Multi-family to Rapid Transit ��������ion Bond

There is a symbiotic relationship between multi-family housing starts and transit projects.

High-rise condo or apartment towers provide ridership on subway and light-rail lines. Easy travel along subway and light-rail lines pumps up demand for housing at transit hubs. They feed off each other.����

That’s why it will be super interesting to discover the degree to which the pandemic, and the shift to working more from home, will impact commuting patterns long term.

Prior to the pandemic, nearly every major city in the U.S. and Canada was planning new or extended rapid transit routes. The time frames for some of these capital spending proposals will be shifted further into the future.

In such instances, the delivery schedules to bring on some new highly-populated residential communities will also be elongated.

Graph 1

Graph 2

Graph 3

Graph 4

Graph 5

Graph 6

Graph 7

Graph 8

Graph 9

Graph 10

Graph 11

Alex Carrick is Chief Economist for ��������Connect. He has delivered presentations throughout North America on the U.S., Canadian and world construction outlooks. Mr. Carrick has been with the company since 1985. Links to his numerous articles are featured on Twitter��, which has 50,000 followers.

Recent Comments

comments for this post are closed